Q2 Catalyst Tracker

Some names that I am watching in the upcoming quarter

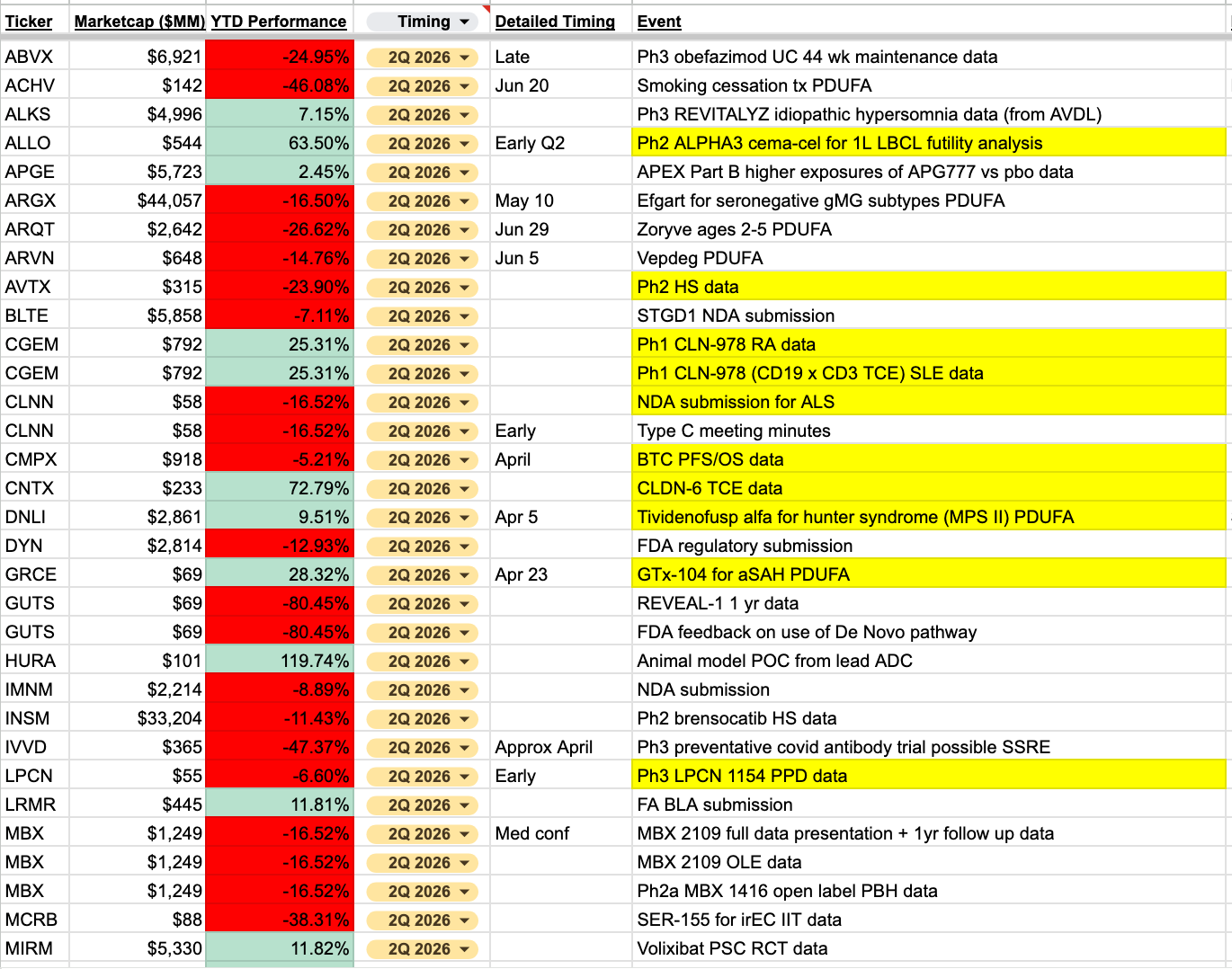

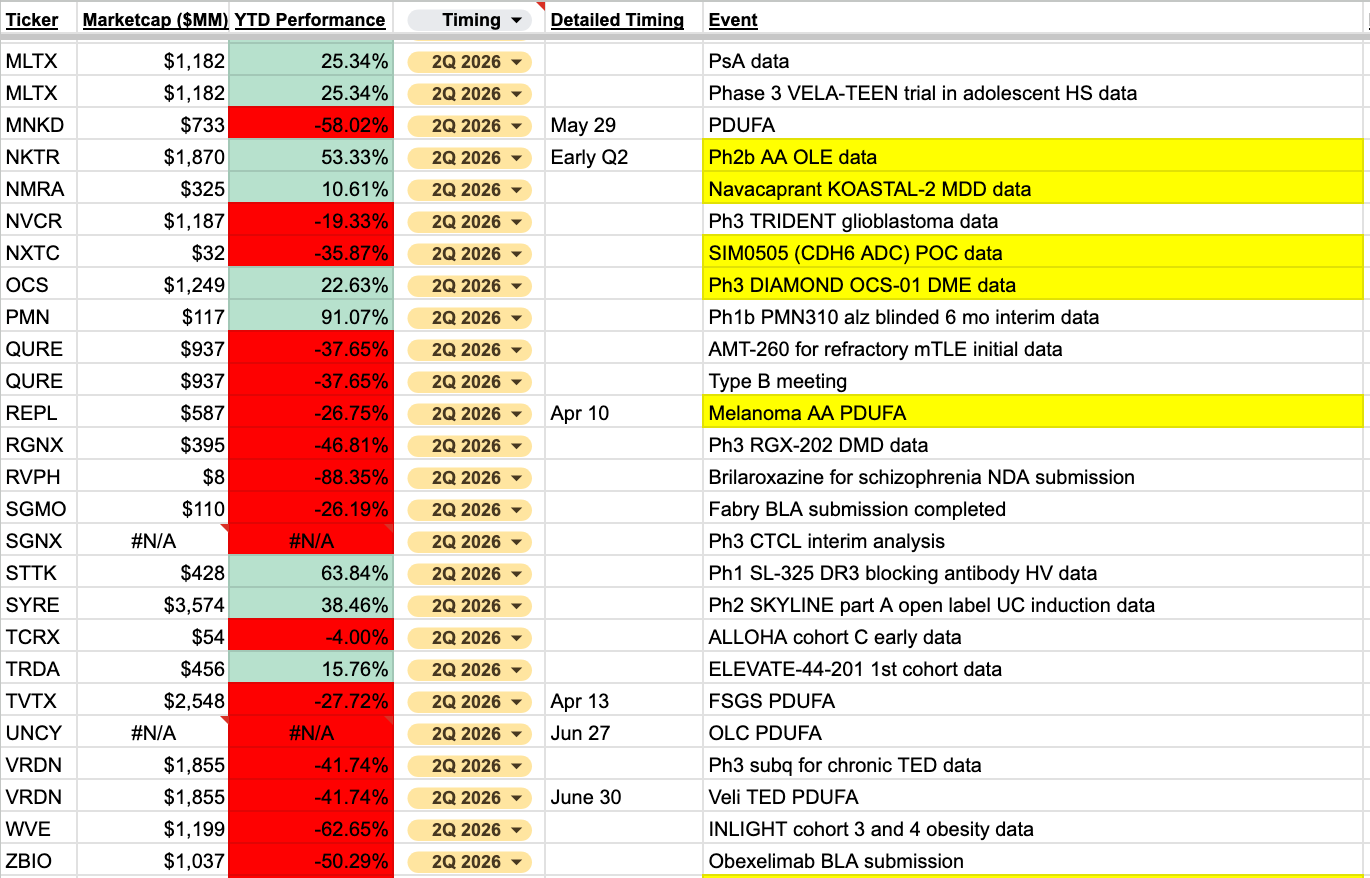

My catalyst sheet has been updated to include over 550 events for this year. I’ll post Q2 events here for all to see, including some highlighted that are most interesting to me. The link to the full sheet is available at the bottom for paid subscribers.

I’m most interested to see what happens with the slew of regulatory decisions coming in April. With Vinay Prasad leaving CBER (again), I think this next round of decisions will give us a clearer picture of how to be thinking about some of these regulatory events. To me, it’s a bit too murky as things stand to know whether to lean toward expecting the status quo, or some potential reversals of prior positions.

In April, we get to see decisions across both the drug and biologic divisions. Specifically, REPL’s 2nd attempt at accelerated approval for melanoma, TVTX’s potential indication expansion to use sparsentan for FSGS, as well as GRCE’s aSAH PDUFA, which appears to be more of a CMC-related debate that I have not followed. DNLI’s MPS II early approval (with possible readthrough to SPRB), is one potential example of the environment becoming slightly more relaxed.

Given the prior controversy around REPL, the reporting around who was responsible for the rejection, as well as all the FDA turnover, it will be fascinating to see what happens here. Handicapping this on the political side seems like too much of a pain to partake in for me, as I can kind of see it both ways. I’d rather just remain on the sidelines and watch it play out.

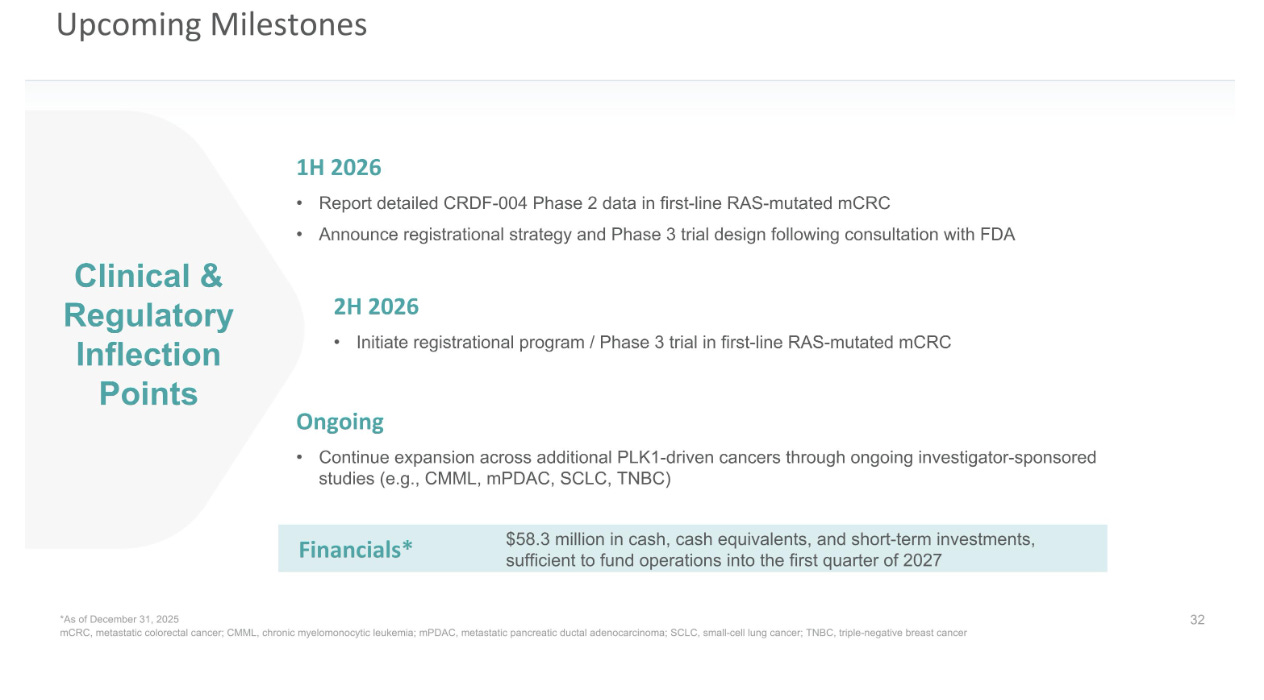

There are a handful of clinical catalysts that I believe are worth more attention. Many of you already know my thoughts on CRDF’s onvansertib, and they are set to present PFS data from their controlled trial in the first half of this year.

In my view, this could be a highly binary setup. They will either present compelling data that lets them secure funding to run the ph3 trial… or they will not. In their latest cut, they were forced to resort to slicing up the data by chemo subgroup. Generally, these types of arguments for chemo-specific synergies don’t pan out. ARAV comes to mind as one example. Considering the upside case, I’m not really sure what they can show that would be exceedingly promising here. Strong PFS data from other arms that doesn’t correlate with ORR will raise questions about the big picture story here. There will be questions about which endpoint is more reliable, as well as how reactive any proposed understanding of how the drug works continues to be. Strong PFS data from the one dose-level and chemo type with promising ORR should be relatively expected. Questions would remain about the validity of the chemo stratification, which is why the stock wasn’t up on the ORR data in the first place. Most versions of this data cut seem likely to be underwhelming, or at best, confusing. Maybe “confusing” is broad enough that they can get a deal done and run the program to completion, but I think consensus would still be a very low probability of success. I haven’t figured out exactly what I want to do here yet, but I see it being a tough road ahead.

CNTX will be presenting initial POC data for their CLDN-6 TCE. There is some external POC for the target, but it will be interesting to see if they can deliver in TCE form.

NMRA is more of a VTYX indirect trade now, I assume? I don’t expect any surprises from the remaining KOASTAL readouts, though neither does anyone else from the looks of it. Assuming the NLRP3 asset is bolstering the valuation quite a bit, I don’t think there’s anything to do here.

For the full list of catalysts, check out the link below.